Why Financial Literacy Should Be Taught in Every UK Secondary School

Imagine a generation of young adults leaving school without the skills to manage their money, navigate credit, or plan for their future. This isn’t a dystopian fiction; it’s a looming reality for many in the UK today. As financial products become more complex and consumer debt rises, the absence of robust financial education in secondary schools is creating a vulnerability gap that threatens individual prosperity and national economic stability.

The Stark Reality: Financial Illiteracy in the UK Today

Financial illiteracy is a pervasive issue in the UK, with significant consequences for young people. According to a 2020 report by the Money and Pensions Service, only 47% of UK children and young people recall receiving meaningful financial education. This gap in knowledge leaves them ill-prepared for the financial decisions they will face upon entering adulthood.

The consequences are already visible in the growing problem of ‘buy now, pay later’ debt among young adults. These services, often marketed seamlessly on social media and online shopping platforms, encourage immediate gratification without a clear understanding of long-term costs and debt traps. Without a solid grounding in financial principles, young consumers are more susceptible to poor credit decisions, high-interest loans, and unsustainable spending habits that can haunt them for years.

Beyond the Maths Textbook: What Real Financial Education Means

True financial education extends far beyond the theoretical probability problems found in GCSE maths papers. It involves practical, applied learning that equips students with the tools to navigate the real-world financial landscape. This means teaching budgeting, understanding the annual percentage rate (APR) on credit cards and loans, comprehending student loan terms, and exploring the psychology of spending and advertising. These topics are ideally situated within the Personal, Social, Health and Economic (PSHE) education framework, which aims to develop life skills for modern Britain.

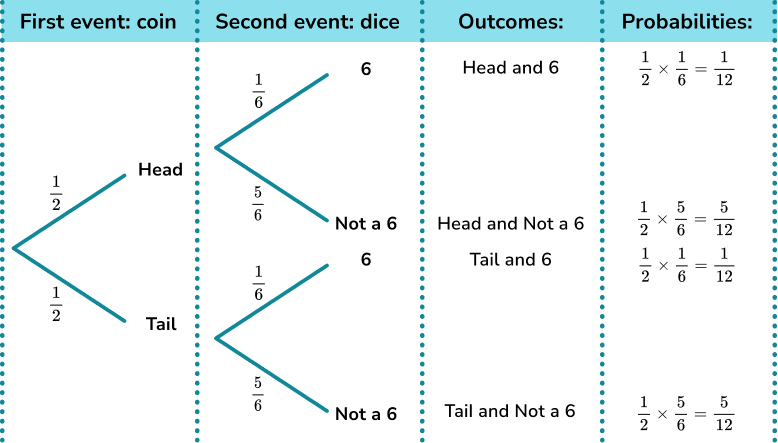

From Probability to Pounds: Applying Maths to Real Life

While GCSE probability math teaches students about chance and outcomes, financial literacy requires applying these concepts to monetary decisions. For instance, understanding the probability of a certain return on an investment or the risk associated with a financial product is crucial. Real financial education bridges this gap, showing how mathematical concepts directly impact personal finance, from calculating compound interest on savings to assessing the true cost of a loan over time.

Core Life Skills: Budgeting, Saving, and Critical Consumption

At its heart, financial literacy is about mastering core life skills. Students need to learn how to create and maintain a personal budget that accounts for income, essential expenses, and savings. This skill set transforms abstract numbers into a practical framework for responsible adulthood. Effective financial education should empower them to:

- Set realistic short-term and long-term savings goals, whether for a first car, university, or a deposit on a home.

- Become critical consumers, able to decipher marketing tactics, compare financial products, and understand the difference between needs and wants.

- Navigate the complexities of taxes, pensions, and insurance, which are often overlooked until adulthood.

The Ripple Effect: Benefits for Individuals and Society

Investing in financial education yields dividends that extend far beyond individual bank accounts. It fosters a more capable, confident, and economically resilient population.

Empowering Personal Wellbeing and Confidence

Financial stress is a significant contributor to mental health issues. The UK charity Mind highlights strong links between debt and mental health problems, including anxiety, depression, and stress. By equipping young people with the knowledge to manage their finances effectively, we can reduce this source of strain. Financial capability empowers individuals, giving them confidence and control over their lives, which is fundamental to overall wellbeing.

Building a More Financially Resilient Britain

On a societal level, a financially literate population is better equipped to withstand economic shocks, contribute to stable markets, and make informed decisions that support a healthy economy. It reduces the burden on public services strained by debt-related issues and fosters a culture of saving and investment. In essence, it builds a foundation for a more prosperous and secure nation.

A Critical Defence: Gambling Maths and Financial Literacy

In an age where young people are bombarded with advertising for online betting platforms, teaching the mathematics behind gambling within a financial literacy framework is not controversial—it’s a vital form of harm reduction. This approach demystifies the industry and arms students with critical analytical tools.

Using Probability to Demystify Risk

Teaching gambling math, such as calculating expected value or understanding bookmaker margins, shows students that gambling is not a pathway to wealth but a probabilistic exercise where the house always has an edge. By applying GCSE probability concepts to real-world betting scenarios, students can objectively see the long-term certainty of loss, transforming gambling from a game of chance into a lesson in statistical reality.

Framing Gambling as a Cost, Not a Chance

Within financial education, gambling can be framed as a discretionary expense with a negative expected return, similar to paying for entertainment. This perspective encourages students to view money spent on betting as a cost, like buying a cinema ticket, but with the added risk of potential addiction and significant financial harm. It promotes responsible decision-making by highlighting budgeting for such activities and recognising the signs of problematic behaviour.

Making It Happen: Challenges and Pathways Forward

Despite the clear need, integrating comprehensive financial literacy into every UK secondary school faces significant hurdles. The curriculum is already crowded, and many teachers feel under-equipped to deliver specialist personal finance content. Currently, the National Curriculum in England includes financial education in Maths and Citizenship, but provision is often inconsistent and non-statutory in all key stages.

Overcoming Curriculum and Training Hurdles

For financial education to be effective, it must be statutory, consistently delivered, and properly assessed. This requires dedicated curriculum time and investment in teacher training. Subject knowledge enhancement courses for maths, PSHE, and citizenship teachers are essential to build confidence and expertise in delivering financial content. Schools need clear guidance and high-quality, ready-to-use resources to integrate these topics seamlessly.

Learning from Successes: Young Enterprise and Beyond

We are not starting from scratch. Successful programmes already demonstrate what is possible. Young Enterprise, a leading UK charity, delivers impactful financial education programmes in schools, combining practical activities with volunteer mentors from the business world. Other organisations, like Young Money, provide frameworks and resources that schools can adopt. Scaling these proven models, with government support and funding, is a practical pathway towards universal financial literacy.

We must act now to ensure that every young person in the UK is equipped with the financial knowledge and skills they need to thrive in an increasingly complex world. By making financial literacy a cornerstone of secondary education, we can empower a generation to build secure futures, reduce mental health strains linked to money, and foster a more economically resilient Britain. The time for debate is over; the time for action is here.

Post Comment

You must be logged in to post a comment.